By Bahle Gama

According to the FNB Economics Weekly from the South African FNB Economics team, inflation was noted to be at 3.2 per cent in November and project a steady lift going into 2025.

But not surpassing 4 per cent.

“This trend is supported by positive base effects and contained underlying inflation,” reported the team.

It further reported that third quarter inflation expectations fell by 0.2ppts to 5.1 per cent for 2024 and 4.8 per cent for 2025.

Meanwhile, 2026 and five-year-ahead expectations fell by 0.1ppt to 4.8 per cent. As headline inflation continues to soften, we should see further slowing in backward-looking expectations.

The risk to this outlook is rising fuel prices.

RELATED: We followed all regulatory obligations – FNB

Mining production expanded by 4.7 per cent year-on-year, a marked improvement from the 0.3 per cent year-on-year increase in August.

According to the FNB team, seasonally adjusted mining output, which aligns with the official quarterly GDP calculation, rose by 3.8 per cent month-on-month following a 3.3 per cent gain in August.

Manufacturing output, not seasonally adjusted, contracted by 0.8 per cent year on year in September, following a 0.8 per cent year-on-year contraction in August.

Seasonally adjusted output was flat (0.0 per cent) after a 0.7 per cent month-on-month decrease in August, contrasting with the manufacturing PMI business activity index, which rose to 53.1 points in September from 34.6 in August, indicating potential expansion.

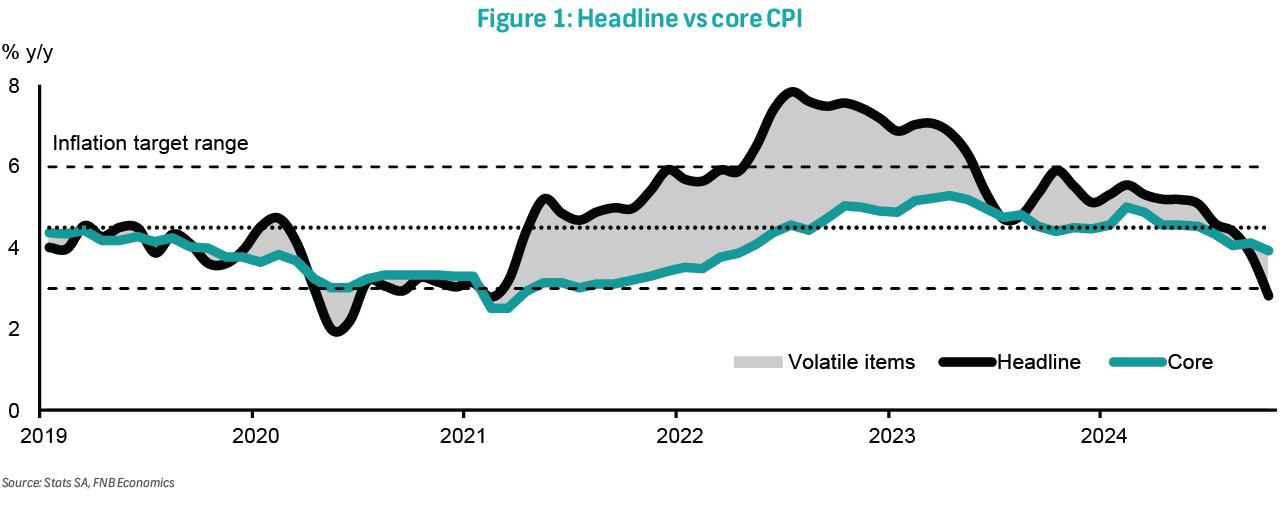

Meanwhile, consumer inflation dipped below the inflation target band in October, posting 2.8 per cent year on year from 3.8 per cent in September.

Headline inflation recorded monthly deflation of 0.1 per cent, as marginal contributions from core and food items were outweighed by fuel deflation.

Core inflation slowed to 3.9 per cent year on year, from 4.1 per cent, with a monthly increase of 0.2 per cent. Food and non-alcoholic beverages inflation also softened to 3.6 per cent year on year from 4.7 per cent, with monthly pressure of 0.4 per cent.

Fuel prices fell by 5.3 per cent m/m and 19.1 per cent year on year. This outcome should be the trough for headline inflation.

Last month, retail sales growth fell short of expectations and decelerated to 0.9 per cent year on year, down from 3.3 per cent in August.

On a month-on-month basis, volumes fell by 0.8 per cent, down from a 0.6 per cent increase in August.

RELATED: FNB Reports Growth in Product Offerings

Nevertheless, year-to-date retail sales have increased by 1.3 per cent compared to the same period last year, indicating a gradual improvement in the consumer environment.

In the second quarter of 2024, formal non-agricultural employment rose by 40, 000 jobs (0.4 per cent), mainly driven by a 90 000-job increase in community services (3.1 per cent).

Year-on-year, employment fell by 144 000 (-1.3 per cent) but has increased by over 500,000 since the second quarter of 2019, reaching 10.7 million workers.

Meanwhile, gross earnings declined slightly by-0.5 per cent quarter-to-quarter but were up 3.9 per cent on a year-on-year basis.

With reduced policy uncertainty and improved economic sentiment, growth and job creation are expected to accelerate.

Producer inflation entered deflationary territory in October, with prices falling by 0.7 per cent year on year.

This marks a significant and prolonged moderation from the peak of 18 per cent recorded in July 2022.

On a month-on-month basis, prices also declined by 0.7 per cent, the fifth consecutive month of contraction.

Excluding petroleum-related products, producer inflation stood at 2.7 per cent year on year and recorded a marginal decline of 0.2 per cent m/m.

Intermediate producer inflation, which reflects manufacturer input costs, rose to 5.5 per cent year on year in October from 4.8 per cent in September, largely reflecting base effects as a monthly decline of 0.4 per cent was recorded.

In the third quarter of 2024 the index surged to a new eight-year high of 50 index points, rebounding from 44 points in the second quarter.

The improvement was primarily driven by a significant recovery in profit margins, reaching their highest level since 2008.

While activity growth moderated slightly compared to the previous year’s peak, the survey indicated increased tender activity and growing intentions to expand employment.

“Nevertheless, respondents continued to express concerns about the negative impact of the construction mafia and government inefficiency on the sector,” reported the team.